Happy Sunday, friends! Hope you’ve all had a great weekend.

I want to review something that analysts and members of the financial media have been keen on declaring — a new commodity “super-cycle” that coincides with the narrative of unsustainable inflation and a dollar depreciation. The narrative is exciting and scary. We can blame the Fed, government spending and anything else we’d like.

Before we dive into the charts, we should note that the narrative directionally aligns with the themes we have outlined — higher yields, strong commodities and a relatively weak U.S. Dollar. While those themes have played out nicely, we haven’t outright called for a major secular shift.

Much of what we have seen so far appears to be the same cyclical changes that follow every economic upturn — cyclicals outperform defensives, long rates move up faster than short rates (the yield curve steepens), economic activity comes back, etc. Secular changes are structural, long-term changes in the economy and the markets. Cyclical changes are shorter, more normal changes as the economy ebbs and flows.

fixed income

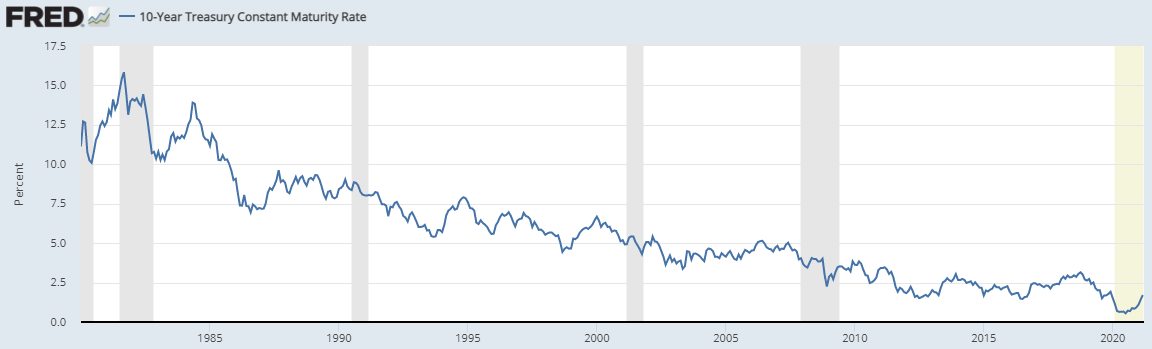

An example of a secular change is the longer-term downtrend in interest rates following the inflation scare of the 1980’s. The chart below shows that long-term trend. Notice the cyclical gyrations up and down within the longer term move down.

While we have been calling for higher rates since the 10-Year Treasury Rate broke out above 0.95%, the larger downtrend from the early 80’s still persists. That doesn’t mean there isn’t plenty of potential upside remaining.

Here’s the daily chart of the $US10Y we have been using. Above 1.465% still offers the opportunity to see 1.80% or even 2.15% on the 10-year note.

commodities

Commodities have been incredible off the COVID lows but there is some work to be done before such bold claims of a “super-cycle” can be made.

Here’s the chart of the Thomson Reuters Core Commodity CRB Index ($TRJEFFCRB). You can see its had some weakness near the trendline from the Great Financial Crisis (“GFC”). Personally, I would like to see us breakout and move onto test the $207 where the commodity rallies of 1997, 2001, and 2018 fizzled out.

Given its large proportion of the Index, crude oil is a huge part of the picture. Unsurprisingly, crude oil futures ($CL1!) ran into some weakness this week at the pre-COVID highs around $65 per barrel. We’d like to crude retake those levels to keep the CRB Index pushing higher.

Dr. Copper is another important piece to the puzzle. We have been extremely bullish on copper futures (HG1!) since it took out our $3.61 level with a target of $4. Let’s see if it can hold for a run to all-time highs around $4.65.

Agricultural commodities ($DBA) are also worth noting. As the chart below shows, we are still within the context of a larger downtrend from the GFC. The ags are trying to hold up above the pre-COVID highs around $17. Above there is another positive.

currencies

The U.S. Dollar Index ($DXY) has been among the most discussed charts since I began writing because of its relationship with the other themes — commodities, emerging markets, etc.

In earlier posts, $89.9 was called out as a key level for a potential reversal. Sure enough, that level has held up as support several times. Right now we are back in the trading range between $89.9-$101.8 that has contained all price action since late 2014.

If we zoom in to the daily chart we can visualize the more recent action. Keep an eye on a sustained move above $92.3 for a confirmed reversal within this larger range.

We can also use the emerging market currencies basket as a gauge on the dollar strength and weakness. Here’s the $CEW chart we have been using. Still battling the larger downtrend and below the pre-COVID highs.

takeaway

While the new narrative of hyperinflation is directionally aligned with our recent investment themes and biases, the price is going to be the ultimate arbiter or truth. The narrative may ultimately come to fruition but I’d prefer to let the charts prove it to us.

Secular changes are inherently long-term, so I don’t see the need to make bold declarations as soon as possible. Changes in long-term trends often play out over long timeframes.

Thanks for reading! As always, let me know what you think and feel free to share this with anyone you think may be interested.

Cheers!